This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Menu pricing isnt just about covering costsits about finding that sweet spot where profitability, customer perception, and operational reality meet. Set prices too low, and youre leaving money on the table. Most operators aim for food costs to be around 28-35% of the menu price, though this can change from restaurant to restaurant.

These issues have translated to the industry’s insurers as well – causing even more headaches for restaurant owners. The restaurant insurance market has seen rising costs to insure and as a result, carriers have come and gone from the market.

Restaurant owners looking to purchase an existing license can face prices up to $1 million depending on demand. A beer and wine license allows restaurants to craft a unique cocktail menu featuring wine-based liquors without the need for liquor insurance or the extensive paperwork associated with a full liquor license.

Of course, running a restaurant is difficult, wholesale prices of ingredients have risen dramatically since the pandemic, labor costs are out of control, and landlords have no mercy when it comes to establishing lease arrangements. So, are we pricing ourselves out of the market? This is not a place where restaurants want to live.

The former are entitled to benefits such as minimum wage, overtime pay and workers’ compensation insurance. Independent contractors, meanwhile, may not get these benefits in exchange for having more freedom and control over their work, while holding responsibility for their own taxes and insurance.

In this changing environment, the right and adequate amount of insurance protection has never been more important. There’s a price for the unrelenting barrage of natural disasters, and it’s making excess liability insurance hard to find above standard liability limits.

What may be overlooked within it are risk and insurance issues. Many franchisors have dedicated staff in charge of maintaining the FDD, although tech solutions are increasingly available, offering efficient, integrated and customizable tools for managing insurance and compliance requirements. And there’s a lot of value to that.

Odds are you understand why your auto insurance premium changes. As you age and become a less risky driver, your insurer is exposed to less risk, and your rates drop as a result. Below, we’ll explore some common drivers of bar insurance costs. Reinsurance, to put it simply, is insurance for insurers.

Longer term savings opportunities will take a concerted effort, and these are areas for review: Self-insured versus fully insured : Plans with more than 150 employee participants are likely strong candidates for self-insurance; and those between 100 and150 employees may also find self-insurance attractive.

Restaurant insurance is complicated. Just as owners have to play many roles in management, marketing, and menus, their insurance has to protect their finances, patrons, and employees. And who has the time to read a 100-page insurance policy? These are often excluded from standard policies and be potentially costly.

On a basic level, stop loss insurance provides protection against catastrophic or unpredictable losses. A basic rule of insurance is that over time, the less insurance purchased will result in a lower cost. Stop Loss Coverage Is Risk Management. a lower deductible).

This is the appropriate strategy for a smaller operator with a single restaurant or with a limited number of restaurants that has to be fully insured. The only factors that have to be considered for this option are price and the use of plan designs that are appropriate for the sector. Then look at their costs.

On Menu Ingredients We predict the rise of “bougie” ingredients like caviar, lobster and truffle popping up at restaurants at more affordable prices and in more casual settings like fast casuals and QSRs. I am concerned that rising insurance costs may force some chains to exit the market. Golden Corral is one.

Rent, food, labor, utilities, and insurance are prime examples. Increasing your prices may prove beneficial : You might even consider adding a special ingredient to some of your low-priced items. Perhaps you can increase the price of the original item, like a premium side, or see if you can bundle them with more expensive items.

Examples include: Rent or mortgage payments Insurance premiums Loan payments Salaried employees (like general manager or executive chef) Because theyre consistent, fixed costs are easier to budget for, but that also means theyre harder to reduce without significant structural changes.

Low-power solutions draw much less power than higher-price cellular or Wi-Fi-enabled solutions to transmit data, which means devices last longer without the need for replacement batteries, resulting in a lower total cost of ownership. Each year, insurers pay out $2.5 billion for water damage claims.

Among the reasons restaurants fail (poor location, inadequate marketing, lack of staff and inventory control, uninspired menu, unreasonable pricing), customer theft is rarely on the radar. ” Some restaurateurs consider this the price of doing business – even a form of marketing.

Insurance Coverage for COVID Claims Largely Rejected by Appellate Courts : Throughout the country, appellate courts are reviewing insurance coverage lawsuits brought by restaurants who were forced to close due to COVID-19 pandemic shutdown orders. Oregon Mutual Insurance Co., Litigation.

In recent years, medical technology has been driving trend, but in today’s economic environment, medical providers are raising prices. In 2021, smaller plans that are often fully insured (fewer than 500 participants) saw a 9.6-percent Additionally, a bubble has emerged due to deferred care. percent rate of increase.

Restaurants have faced labor shortages, supply and equipment shortages, and climbing food prices, with no past playbook on how to navigate the crisis. These include sign-on bonuses, higher wages and the offering of health insurance. Looking ahead : Equipment manufacturers estimate that prices will stop climbing sometime in 2022.

Fixed costs Fixed costs are expenses that remain constant, including rent, insurance, and utilities. If transferring isn’t an option, you can try to reduce other fixed costs like insurance premiums. If transferring isn’t an option, you can try to reduce other fixed costs like insurance premiums.

The premise is that employees (especially those with significant health issues) have difficulty navigating the world of health insurance and, therefore, are susceptible to making poor and inefficient choices. This compares to the average insurance provider score of 57. The piece not yet addressed is cost savings.

Auto insurance. Get car insurance You must establish who is liable in the event of an accident. Drivers must have auto insurance in order to drive their vehicles, thus you must lay-out in the contract if you will be paying for any damages while on the job. Auto is in quality shape. Valid driver's license. Clean driving record.

. – Sophia Goldberg, Founder and CEO, Ansa The big lesson I learned is that I've had to continue to adapt my pricing, because people are still watching their spending. That's why we instituted lower-priced lunch specials and made other adjustments. – Izzy Kharasch, President and Founder of Hospitality Works, Inc.

Lack of health insurance isn’t considered one of the major reasons the hospitality industry has, according to the U.S. One of the major ways to invest in employees is through health insurance, something only about 30 percent of restaurants provide. Bureau of Labor Statistics, a churn rate north of 70 percent.

Another growing risk: nuclear verdicts over dram shop law violations, driving up the costs of liquor liability insurance. It’s a continuing problem into 2024 for establishments that serve, making it critical to have adequate liquor liability insurance. It’s the best way to secure coverage at the best terms and prices.

This number is essential because it helps you determine the price of your food and beverages. This metric helps you measure the amount spent on labor, particularly salaries, worker benefits, insurance, overtime, and payroll taxes. As a rule, this should make up about 1/3 of your total expenses.

When introducing new menu items to a menu category, they must be priced at the average profit from that menu category + the recipe cost of goods sold (COGS), and then rounded off to the next half dollar. Round up to the next half dollar and the menu price should be set at $12.50 to ensure you haven’t compromised profitability.

Over the past year or so, coffee prices have been steadily increasing. The first sign that prices would increase was a sudden frost which hit some of Brazil’s major coffee-producing regions in late July 2021. Since then, prices have consistently remained above the US $2 mark. Exploring prices and costs at origin.

Provide great benefits, 401k, life insurance, etc. However, with historic low-price points on food along with the typical financial structure of a restaurant, it does not allow restaurants to pay out truly reasonable livable wages in urban cities.” ” One way to do so: increase menu prices.

Low-power IoT solutions, in particular, offer added benefits because they draw much less power than higher-price cellular or Wi-Fi-enabled solutions to transmit data, which means devices last longer without the need for replacement batteries, resulting in a lower total cost of ownership. Each year, insurers pay out $2.5

Not only do you have to manage many costs including, labor, equipment, and food—but you have to do it while dealing with inevitable price increases. Fixed costs include rent, mortgage, salaries, loan payments, license fees, and insurance premiums. Indeed, controlling restaurant costs is one of your biggest challenges.

Lille Allen Six chefs and restaurant owners from across the country explain why restaurants feel so expensive right now, and how they’re coping with high prices and customer complaints Dining out involves calculating the intangible: What is hospitality worth to you? This isn’t a problem of one city or class or demographic.

It is affected by seasonality, market prices, and even pop culture. Determine your ideal menu price Multiply your plate cost by the food cost percentage to reach a target menu price. per serving Consider variables You can price the burger at $9.25 (rounding up) and make a profit on it. Food prices have been on a steady 2.6

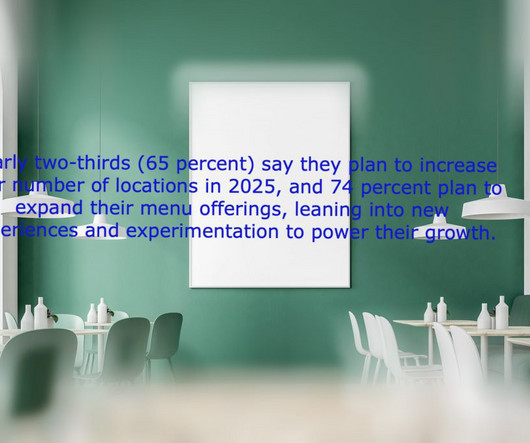

The research found that businesses worldwide – particularly restaurants – intend to experiment more in 2025, especially with customer retention programs like loyalty, as they face the triple challenge of sustained high inflation, shrinking consumer wallets and the need to raise prices across the board. percent decrease in claims.

Deduct the cost, not staff time or full price. Staff pay: salaries, insurance, bonuses. Insurance: property, liability. Accounting Tip: Split costs in your accounting software. Use 75% repairs, 25% capital improvements. Charitable Donations: Give and Get Back Donating extra food? Feels good, saves cash. Rent: your spaces lease.

The importance of the price of offering lowered from 78 percent to 50 percent. Prioritizing price amidst COVID-19 fell by almost half among those ages 60+, from 78 percent considering it a top-three factor prior to the outbreak to 41 percent now. For those who would choose to travel, purchasing insurance is key. A total of 71.6

Now here is the kicker – excellence has very little to do with the price you charge or the type of product or service you provide. Create a similar checklist for every product on your menu, regardless of the type of operation or the prices on you charge and you will find a path from mediocrity to excellence.

This compares to Brand drug pricing that has increased 36 percent in the last five years. It’s also is not viable to carve Rx coverage out of a fully insured contract due to the lack of stop loss availability. Of even greater concern, specialty drug spending is increasing 10 to 15 percent annually.

The primary response was menu price increases, with nearly 61 percent of respondents adjusting prices to cope with the new reality. Despite brands’ value focus, average price continued to increase, up +2.6 Traffic stayed in positive territory (+1.3 percent YOY. Net sales were up 4.9 percent as a result.

Ideal menu price. Your CoGSs is an essential number to have when determining your menu prices, inventory and impacts your net profit margin. It also plays a key factor in pricing your menu. To get your restaurant's break-even point, you'll need the following: Total fixed costs, like rent, salaries, and insurance.

Marketing Plan : detail your pricing structure (e.g., premium pricing), your location, your menu, and the promotional strategies (e.g., This means the bank is partially "insured" in case somebody is unable to repay them. The best way to do that is by conducting a restaurant feasibility study.

Despite the fact that the pandemic put all of these workers in grave danger while they were offered none of the unemployment insurance benefits given other workers, the gig companies were able to use expensive and sophisticated propaganda to confuse voters. Vianne recalled using DoorDash first. Go online ASAP to cash in!”

Many restaurants already had to buy heaters at inflated prices, given the increased demand as temperatures started dropping last fall. Filing an insurance claim — which requires a police report — can help make up for some of the lost income and stolen property cost. Marrow’s stolen property was valued at about $1,400.

We organize all of the trending information in your field so you don't have to. Join 49,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content